The trend in the European gas market reversed and turned bearish on Friday after a number of bullish movements seen earlier in the week.

While the upturn of the past days was being driven by reduced supply amid an outage at Norway’s Troll facility, flows increased again on Friday. Energi Danmark said that the market again focuses on the expectations that the gas storage across Europe will likely be full at some point during autumn.

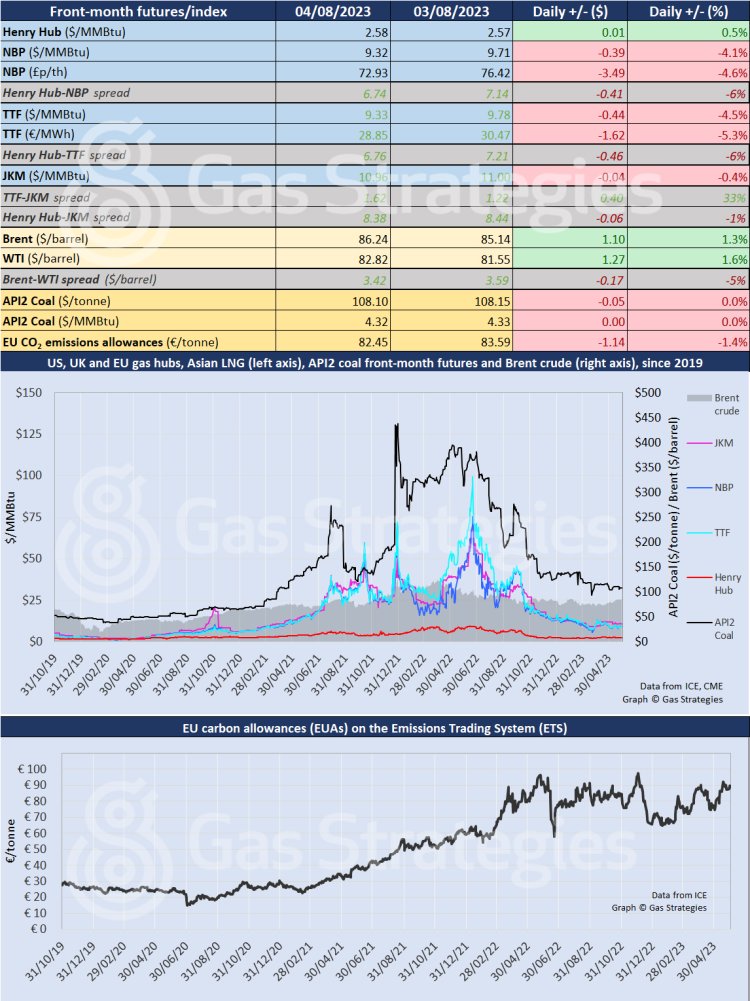

GIE data showed European storage was already 87.1% full on 5 August, ahead of the schedule of EU’s filling targets.

As a result, TTF saw a 4.5% decline to USD 9.33/MMBtu and NBP fell 4.1% to USD 9.32/MMBtu.

Meanwhile, JKM saw a minor 0.4% downtick to USD 10.96/MMBtu. This came amid reports that China’s demand for LNG rebounded in July, with ICIS LNG Edge data revealing a 23% LNG import volume jump from the same month last year, which were also above 2021 levels.

In the US, Henry Hub saw a 0.5% rise to USD 2.58/MMBtu. This followed as the EIA reported inventory injections at the lower end of the forecast range, of 14 Bcf, nearly three times less than the volumes injected in the prior year.

Oil rose by over 1% on Friday to record a sixth consecutive week of gains, after top producers Saudi Arabia and Russia extended supply cuts through September, adding to undersupply concerns, according to Reuters.

Brent rose 1.3% to USD 86.24/barrel and WTI by 1.6% to USD 82.82/barrel.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):  Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.